With COVID-19, being declared a pandemic on March 11, 2020, financial institutions have

had to shift most of their resources to mitigate the risks that have arisen.

This has adversely affected important activities, one of which is market

participants’ efforts to detach from LIBOR before its cessation at the end of

2021. As a result, most of the market’s attention continues

to focus on two areas regarding the reform. First, is the pandemic’s

impact on the already-tight deadlines put in place to boost transition progress, as well as

the regulator’s response; second, is the behaviour and robustness of Alternative

Risk-Free Rates under a stressed environment. In particular, there are

questions on the robustness of the Secured Overnight Financing Rate (SOFR) in

relation to USD LIBOR.

SOFR is an overnight rate calculated daily using actual transactions

in the wholesale interbank funding market and collateralised by US Treasury

Securities. In this respect, SOFR is very different from USD LIBOR, which is an

unsecured term rate set by a panel of banks.

LIBOR is not based on actual transactions but rather on the rate that

banks are willing to lend to each other, which results in bank credit risk

being embedded in the rate’s value. Because of these fundamental differences, it is interesting

to compare the behaviour of both rates under the current stressed market environment.

It is the Alternative Reference Rates Committee’s[1](ARRC) opinion that SOFR

can be characterised as a robust rate based on several aspects. Amongst others,

SOFR is more robust than LIBOR due to its minimal exposure to manipulation

based on actual transactions. Furthermore, a rate’s robustness can be assessed on the

volatility it depicts during times of stress and its adherence to the economy’s

evolution. The adherence to the economy’s movements can be captured by the rate’s

co-movement with other money market rates.

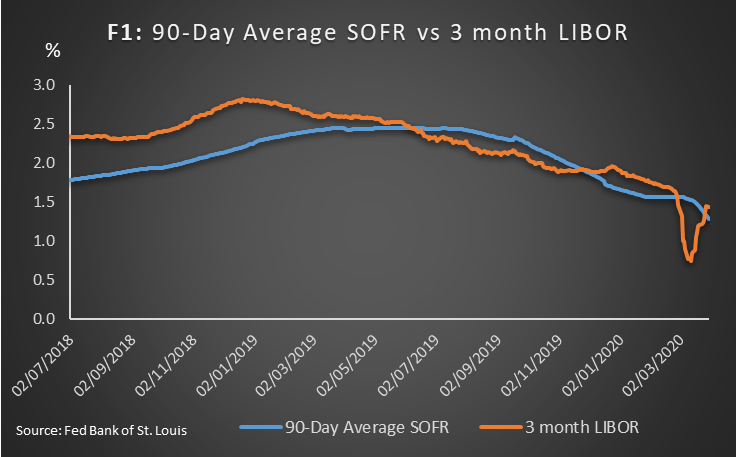

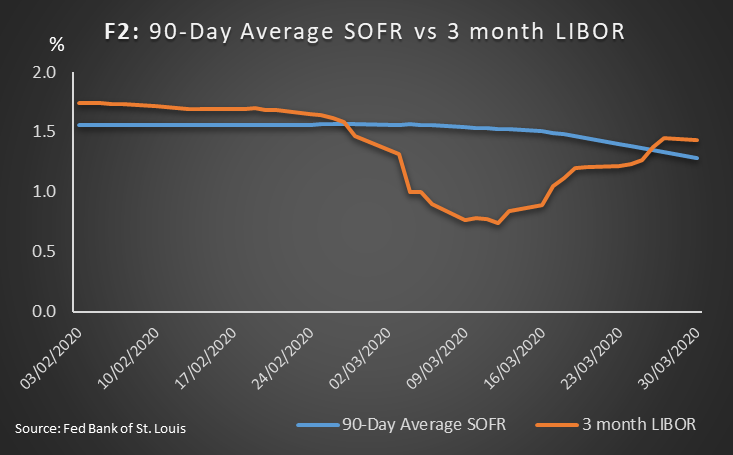

Figure 1 below depicts the 3-month USD LIBOR and the 3-month average

SOFR. Up until February 2020, the rates have followed a similar trend. However,

in March 2020, they moved in opposite directions. USD LIBOR plummeted to a

minimum of 0.74% and then started rising aggressively during mid-March. In

contrast, SOFR followed a slightly downward trend exhibiting little volatility,

as illustrated in Figure 2.

The different movements can be attributed to the credit risk component

embedded in USD LIBOR, with the rate’s aggressive rise after mid-March

explained by an increased perceived risk in the banking system. Also,

the calculation method of the 3-month average SOFR smooths out volatility,

which inhibits strong fluctuations. In addition, SOFR seems to be pulled by the

FED’s actions. First by the Quantitative Easing (QE) Program whereby the

Bank buys Treasury Securities and Mortgage-Backed Securities and, second, is the

$500bn offering in overnight repos. This flood of liquidity seems to have

driven the SOFR to low levels, which is perhaps not unexpected due to the rate’s

link with US overnight repos collateralised by US Treasury Securities.

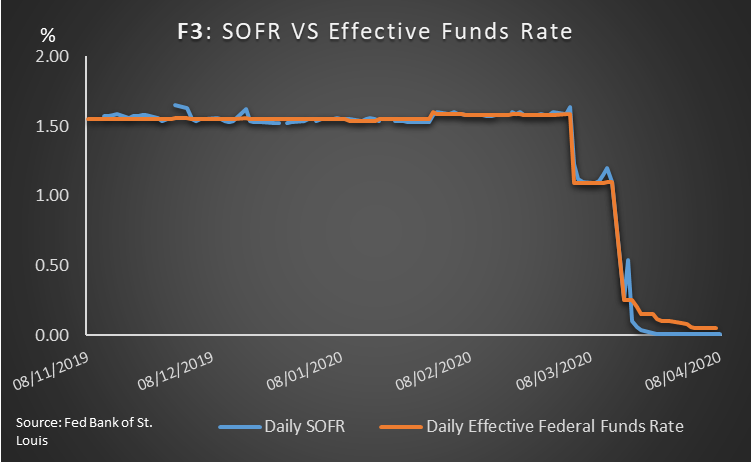

The average 3-month SOFR appears to be more robust than 3-month

LIBOR due to the lower volatility it has exhibited during the crisis so far.

Another argument in favour of SOFR’s robustness is the rate’s high correlation with the Effective Federal Funds Rate, as

illustrated in Figure 3. SOFR exhibited a slight lag before reaching approximately

the same level as the Fed Funds Rate, as shown by the positive spread between

the two rates during March. Evidently, the FED’s actions have managed to draw down

secured lending and money market fund rates eventually, but not LIBOR.

The Fed’s intervention substantiates

doubts raised earlier in 2020 by a group of mid-size American banks[2] regarding SOFR’s

behaviour during a crisis. The banks argued that during a crisis there is an

increased demand for overnight liquidity, which would lead to a jump in

short-term borrowing rates such as SOFR. This tight relationship between the

repurchase market and SOFR was also observed in September when a spike in the

repo market led to the rate skyrocketing. The Central Bank’s actions have

strongly influenced the rate’s stability during the current crisis, and market participants are

wondering whether the Fed would always be needed to keep the rate stable. If

that is the case, then is the rate as robust as it seems?

SOFR also has further drawbacks that have not gone unnoticed by market participants. These include the lack of a credit component that could be useful for hedging purposes, as well as the absence of a term structure. To add to this, the liquidity of SOFR-linked markets remains much lower than LIBOR’s. In April 2020 the volume traded in SOFR-linked swaps was 100 times lower than the volume of USD LIBOR-linked ones ($12 bn vs $1200 bn[3]).

While it is legitimate to question the robustness of replacement rates such as SOFR, it’s also essential that enough data and liquidity are available to be able to draw firm conclusions. As global economies begin to emerge from the COVID-19 pandemic and banks devote more resources to the transition away from LIBOR, the behaviour and robustness of Alternative Risk-Free Rates will become more evident.

As we enter the final quarter of 2025, political instability and limited growth continue to affect the global economy. However, promising market opportunities are emerging. Banks, insurers and asset managers must be prepared to navigate efficiently in an evolving domestic and cross-border tax environment. In this October edition of the Financial Services Tax Digest, experts […]

IFRS 18 – Presentation and disclosure in financial statements is set to replace the IAS 1 – Presentation of financial statements and will be effective for the period beginning on 1 January 2027. IFRS 18 applies to all entities, including insurance companies. For insurance companies, IFRS 18 follows a series of transformative accounting standard milestones. While IFRS […]

Conducted by David Ciolfi, Senior Manager, Forvis Mazars RegCentre On 12 May 2025, the Basel Committee issued a landmark statement reaffirming its commitment to finalise the full implementation of Basel III in all jurisdictions “in full and consistently and as soon as possible”[1]. This position comes amid growing tensions between the ambition for a globally […]

Eric Cloutier, Partner, Forvis Mazars Group, took part in the EUFORI panel in September 2025 on ‘Simplifying EU banking regulation and supervision; priorities and next steps’. The session was moderated by John Berrigan, Director-General at DG FISMA, with esteemed panellists including senior policymakers and supervisors such as José Manuel Campa (Chairperson, EBA), Nathalie Aufauvre (Secretary […]

A snapshot of the sustainable finance landscape in APAC In spite of a slowdown in the APAC sustainable finance market in 2025, momentum remains strong in key pockets. Sovereign issuances are setting the tone for private sector participation and strong local currency markets are bolstering domestic growth, encouraging the participation of APAC’s growing ecosystem of […]

Insights from George Lagarias, Chief Economist, Forvis Mazars Economics Hub. The financial services sector is poised for growth due to deregulation and lower interest rates, enabling banks to expand loan books and recapture market share from private investors. However, global economic challenges, including trade wars, persistent inflation and high debt levels, cloud the outlook. Risks […]

As the saying goes, “the only constant in life is change.” As we enter the third quarter of 2025, global economic uncertainty continues to escalate. President Trump’s pause on “reciprocal” tariffs is set to expire on 8 July 2025. Currently, the U.S. has only reached trade deals with the UK and China. However, negotiations with […]

To harness the potential benefits of AI safely, financial institutions must ensure that they have appropriate guardrails in place to allow safe innovation. The EU’s AI Act will help shape how institutions govern artificial Intelligence across functions. Boards must focus on ensuring that AI risks are identified and addressed across the development, procurement and use […]

Sanctions compliance has rapidly evolved from a niche area of regulatory focus into a critical and high-risk concern for financial services firms. As geopolitical tensions rise and sanctions regimes become more expansive and ever changeable, firms operating across borders must navigate an increasingly fragmented and high-stakes landscape. In advance of the launch of Forvis Mazars’ […]

As ESG and climate risks climb the supervisory agenda, financial institutions face rising expectations from both UK and EU regulators. This article compares the evolving approaches of the PRA and EBA—and what firms must do now to stay ahead. In the past six months, the Prudential Regulation Authority (PRA) and the European Banking Authority (EBA) […]

Europe’s capital markets are increasingly integrated — but supervision remains fragmented. Without a more coherent supervisory model, regulatory arbitrage and inefficiencies will grow. A new approach is needed. The EU’s financial market supervision remains fragmented and misaligned with the depth of market integration achieved through initiatives such as the Capital Markets Union (CMU) and the […]

The reform of the Solvency II Directive, set to be enforced no later than January 30, 2027, introduces new sustainability-related risk requirements. These include (i) the creation of transition plans with quantifiable goals and processes to monitor and address financial risks from sustainability factors in the short, medium, and long term and (ii) an assessment […]

A follow-up to our previous analysis In our previous article – Navigating the new trade war: implications on Expected Credit losses – we explored the rise in provisioning needs triggered by both direct impacts (sector/geography-specific exposure to tariffs) and indirect impacts (macroeconomic degradation influencing model parameters). Through simulations and stress testing, we showed how seemingly […]

Political background Since early 2025, under President Donald Trump’s second term, the United States has escalated tariff actions on a wide array of imports, reigniting global trade tensions. A series of key announcements* has introduced significant volatility into financial markets: *This context is accurate as of 10 April 2025. However, given the extreme pace of […]

In an exclusive interview with Forvis Mazars, Simon Rawson, Executive Director, The Taskforce on Inequality and Social-related Financial Disclosures (TISFD) discusses the work, objectives and approach of the taskforce. Simon explains how the taskforce is about creating a knowledge base, evidence and recommendations on a social-related disclosure framework that could be used for businesses to […]

As Benjamin Franklin famously said, nothing is certain in this world except death and taxes. As we enter the second quarter of 2025, we find great uncertainty – and tax is at the heart of it. The prospect of an international tariff war looms. Although financial services businesses are not expected to be the primary […]

In 2025, the financial services landscape in the Asia-Pacific (APAC) region continues to experience rapid and structural change driven by complex and interconnected risks. These elements are fundamentally reshaping regulatory priorities across the region, prompting diverse responses from national authorities. The region’s vast diversity can lead to regulatory fragmentation, requiring financial institutions to navigate a […]

The DORA (Digital Operational Resilience Act) regulation came into force across the financial sector on 17 January 2025. Unsurprisingly, only a small number of firms affected by DORA have declared themselves completely ready and compliant with all areas of the regulation. The European Supervisory Authorities (ESAs) have affirmed their position on the minimum requirements firms […]

This article was written in collaboration between our Forvis Mazars Economics Hub and Forvis Mazars Global Financial Services Regulatory Centre. In the aftermath of the 2008 Global Financial Crisis (GFC), stringent regulations were developed for the banking and insurance sector to prevent the need for future public bailouts during times of financial stress. Nearly two […]

On 2 December 2024, The Single Resolution Board (SRB) published its work programme for 2025. The Programme sets out the SRB’s main priorities for the next year, alongside the continued and important work on standard operations. An overarching priority is to streamline the resolution planning process and resolution plans to make them more efficient and […]

On 1 October 2024, ESMA published its strategic priorities for 2025: ESMA’s annual work programme. The strategic priorities for this year build on the five-year ESMA strategy for 2023 to 2028, focusing on fulfilling ESMA’s mandates in legislation and expanding upon activities from 2023 and 2024. ESMA’s 2025 strategic priorities are outlined are three strategic […]

On 18 December 2024, The European Central Bank (ECB) published its supervisory priorities for 2025-2027, which reflect the Bank’s medium-term strategy. Forvis Mazars interviewed Patrick Montagner, member of the ECB Supervisory Board, to discuss the ECB’s supervisory priorities for 2025-2027 and the 2025 stress test. The conversation highlights how the ECB is adapting its supervisory […]

On 2 October 2024, the European Banking Authority (EBA) outlined its work programme for 2025, focusing on the continued implementation of the EU banking package (Capital Requirements Regulation (CRR) III / Capital Requirements Directive VI) and the enhancement of the Single Rulebook, which was also a priority in 2024. Additionally, the EBA will take on […]

The Basel Committee work programme for 2025/2026 outlines the strategic priorities for its policy, supervisory and implementation activities for the two-year period. The key themes of the committee’s 2025-2026 work programme include: The work programme builds on its mandate to strengthen the regulation, supervision and practices of banks worldwide with the purpose of enhancing global financial […]

The European Insurance and Occupational Pensions Authority (EIOPA) published its 2025 work programme which is embedded in its revised single programme document 2025-2027. The year 2025 marks the start of this three-year plan. EIOPA’s mission is to protect the public interest by contributing to stability in the short, medium and long term. This mission is […]

Sovereignty raises debate and there is a wide divergence in the way to deal with that topic. The current debate in Europe on the EU Cloud Services (EUCS) High+ criteria is an illustration of the diverse positions existing in that field. Addressing sovereignty as an isolated concept does not make sense. Sovereignty should be addressed […]

In this exclusive interview by Forvis Mazars, Patrick Montagner, member of the ECB Supervisory Board, discusses the ECB’s supervisory priorities for 2025-2027 and the 2025 stress test. The conversation highlights how the ECB is adapting its supervisory focus and practices to address the evolving risks faced by the banks it supervises, including geopolitical shocks, climate […]

As we say goodbye to 2024 and look forward positively to 2025, at Forvis Mazars we know that financial institutions and funds will have to deliver in an evolving complex domestic and/or cross-border tax environment. Banks, insurers and asset managers all over the world may have to capture M&A opportunities and/or deal with some efficient […]

In November 2024, the Network for Greening the Financial System (NGFS) released the latest version (termed Phase V) of its climate risk scenarios. These introduce significant advancements that enhance financial institutions’ accuracy when undertaking climate-related financial risk assessments. Key advancements include the incorporation of a new damage function for physical risk assessment, the integration of […]

As the impacts of climate risks become more pronounced, regulators and the insurance industry are under increasing pressure to refine risk assessment frameworks. This article examines regulatory developments, a critical review of climate scenarios and limitations of models within the insurance sector, the implications of new regulatory developments, and the role of actuaries in establishing […]

In the wake of financial crises, the question ‘Where was the board?’ has become a rallying cry, reflecting the demand for greater accountability within banking institutions. Recent high-profile bank collapses underscore the necessity of robust internal governance frameworks that include a strong risk culture at their core. Supervisors worldwide continue to elevate risk culture as […]

As part of our annual series on “Top risks facing financial service (FS) firms”, we have identified and ranked the key risks for financial services business leaders in 2025. We discuss in the article below the top five areas that FS firms should prioritise in 2025. Our more detailed assessment can be found here, which contains […]

Forvis Mazars proudly participated in the Africa Financial Summit (AFIS) 2024, held from 9-10 December in Casablanca, Morocco, and sponsored the awards ceremony. Below are some reflections on the state of play and future of Africa’s financial sector. In recent years, the world has undergone dramatic changes, challenging the status quo in unprecedented ways. This […]

In November 2024, the NGFS[1] (Network for Greening the Financial System) published phase V of its widely used climate scenarios updated with the most recent economic and climate data, policy commitments, and model versions. This phase V also introduces a new damage function for physical risk assessment. The new damage function incorporates various climate variables […]

Cloud computing has been with us for over 15 years, but we have barely scratched the surface of its potential.[1] Industry Cloud Platforms (ICPs) are cloud-based solutions targeting the specific needs of industry verticals that generic and traditional solutions do not adequately address. These solutions encompass cloud services, applications and data models tailored to meet […]

When the Covid-19 pandemic broke out in 2020, the banks had to make post-model adjustments[1] (or management overlays) to incorporate the impact of this unprecedented situation into the expected credit losses recognised by the banks. While the end of the pandemic should have put an end to these exceptional adjustments, the events that followed (war […]

After several years of significant macroeconomic and geopolitical events such as the Covid-19 crisis, the war in Ukraine, the return of inflation and rising interest rates, the year 2023 seemed to mark a form of stabilisation in the international environment in the absence of any notable new event, despite the continuing uncertainties. How has the […]

The European Supervisory Authorities (ESAs) published the final texts of the DORA (Digital Operational Resilience Act) regulation in July. These definitive texts will come into effect in January 2025, enhancing digital operational resilience and IT risk management for all financial entities. Key takeaways from the final DORA regulation texts In July, the European Supervisory Authorities […]

A day doesn’t seem to go by without there being another sustainability regulation announcement. This article is a whistle-stop tour around selected jurisdictions and provides an update on what has happened in the past few months, what is to come, and what these developments mean for firms. In summary, reporting on sustainability issues is growing […]

In the ongoing digitalisation of the banking sector and the rapid growth of financial technology, banks increasingly rely on third-party service providers (TPSPs), including for some of their critical functions. This dependency introduces significant risks, as banks do not always have direct control over these external entities. These risks are further exacerbated by cyber threats, […]

Traditional methods of tackling financial crime are no longer effective in a world where bad actors use increasingly sophisticated techniques to exploit weaknesses in financial crime controls. With the establishment of a new European regulator, embedding the latest AI-enabled solutions to counter financial crime is of utmost importance. The formation of the Anti-Money Laundering and […]

In today’s dynamic financial landscape, cryptocurrencies and their underlying technology have taken centre stage, attracting both enthusiasts and sceptics. The volatility and potential of digital assets prompt questions about their evolving positions in the traditional financial market. While the promise of decentralisation sparks innovation, ongoing debates on regulation, security, and stability keep the narrative of […]

On 24 February 2024, Ukraine and the rest of the world marked the second anniversary of Russia’s invasion. Despite extensive media coverage of the war and its geopolitical and socio-economic ramifications on Europe and the rest of the world, there is an opportunity for investors to explore the potential in Ukraine. This article aims […]

The role of artificial intelligence (AI) in financial services continues to exercise C-suite minds. Not least, how to balance AI’s benefits to enhance the customer experience and improve back-office operations with the ethical challenges that AI presents. Sparking the debate is how financial organisations can employ AI tools such as machine learning (ML), large language […]

The financial services sector is increasingly looking to technology to help tackle the rising levels of regulation they face. According to the latest Forvis Mazars C-Suite Barometer, the prominence of new technology as a global trend is on the rise in financial services, making it one of the most important issues now topping the C-Suite […]

As financial services organisations increasingly focus on digital transformation, having the right expertise and skillsets is critical. However, it’s not simply a question of human capital. It requires developing a talent strategy that recognises the profound impact technology will have across the organisation. Technologies such as cloud, containers, artificial intelligence and machine learning, internet of […]

Digital transformation now tops the C-Suite agenda of financial services organisations. According to the latest Forvis Mazars C-Suite Barometer, one-third of respondents identified the need to transform company IT as a strategic priority ahead of issues such as sustainability initiatives. While the competitive landscape has been evolving for several years following the arrival of digital-first challenger […]

Optimism in the financial services sector is riding high. According to the latest Forvis-Mazars C-Suite Barometer, 94% of financial services respondents say they’re growing, which is five points higher than the global average and up overall from 92% last year. At the same time, 97% of leaders in financial services predict growth in 2024, up […]

In the aftermath of the Global Financial Crisis, regulators and legislators around the world tried to make sense of its causes and then implement rules to stop it happening again. In the UK, the resulting regulation introduced by the Financial Conduct Authority, FCA, was the Senior Managers Certification Regime, which in its current state, carries […]

In the dynamic world of finance, regulatory updates play a pivotal role in shaping industry practices and safeguarding the interests of stakeholders. From strengthening anti-money laundering measures to fostering transparency in crypto-asset markets, recent months have witnessed a flurry of regulatory activity across various domains. In this comprehensive overview, we delve into the intricate details […]

Operational resilience is the ability of firms to prepare for, prevent, adapt and respond to, recover and learn from operational disruption. It is a complex and multi-faceted challenge for cross-border banks to prepare for and respond to. This is because potential causes of operational failure can enter a firm from several directions and their impacts […]

An EU vs UK vs US perspective Sixteen years ago, the collapse of Lehman Brothers triggered the global financial crisis, which highlighted significant weaknesses in the global banking sector. The oversight of the sector was quite fragmented between jurisdictions, leading to inadequacies in regulation and supervision. In response, the Basel Committee, which sets global standards […]

Differing approaches to Anti-Money Laundering (AML) and Counter-Terrorist Financing (CTF) supervision across the EU have severely limited member countries’ ability to fight efficiently this growing threat. The creation of the Anti-Money Laundering and Countering the Financing of Terrorism Authority (AMLA) is a huge step in addressing this issue. AMLA will be charged with i) supervising […]

Following the 2007-08 global financial crisis, substantial deficiencies were identified in many banks’ risk data aggregation capabilities and risk reporting practices globally. This impacts banks’ ability to make timely risk decisions, creating risks not only for themselves but for the stability of the global financial systems. The Basel Committee responded by developing in 2013 the […]

Financial institutions are faced with several challenges: strong economic pressure, regulatory changes, evolving customer expectations, punctuated by strong competition from fintechs and insurtechs; which rely natively on emerging technologies to offer best-in-class services. To meet these challenges and stand out from fintechs and insurtechs, financial services (FS) companies have invested massively in move-to-Cloud strategies, rapidly […]

Reinforcement Learning (RL) is a branch of Machine Learning (ML) that is still little known to the general public. In this approach, an agent repeats actions and, depending on the result of these actions, receives a reward or punishment in the form of a score. Focussed on maximising the score, the agent adapts the next […]

Africa’s economic potential is hindered by the pervasive presence of illicit financial flows (IFFs), fraud, and corruption, which not only strip the continent of vital resources but also obstruct its path towards sustainable development. The staggering annual loss of $88.6 billion to IFFs, as reported by the United Nations Conference on Trade and Development (UNCTAD), […]

In the ongoing battle against financial crimes spanning money laundering, terrorist financing, and the proliferation of weapons of mass destruction, collaborative efforts in asset confiscation and seizure stand as vital bulwarks. As we navigate the complexities of the financial landscape in 2024, recent advancements, particularly within the European Union (EU), underscore the critical importance of […]

We have identified and ranked the key risks for financial services business leaders in 2024 based on market research, regulatory insights as well as our assessment of the current difficulties facing firms. We discuss in this article the key takeaways for you and your organisation. A more detailed assessment can be found here, which contains […]

We have identified and ranked the key risks for financial services business leaders in 2024 based on market research, regulatory insights as well as our assessment of the current difficulties facing firms. We also highlight the changes in risk rankings compared to last year, justified by global events and new regulations that have surfaced in […]

In the contemporary landscape of insurance, the business model of open insurance, characterised by the strategic opening of insurers’ resources to external collaborators, has been a focal point of discussion. Unlike the banking sector, where regulatory mandates such as the Payment Services Directive (PSD2) of 2018 have compelled the development of open banking practices, insurers […]

Mazars recently hosted a Financial Services INED Roundtable Dining Event in Dublin[1]. Over 50 financial services independent non-executive directors (INEDs) attended, from banking, asset management, funds and insurance entities operating across the EU and UK. The roundtable focussed on the challenges facing INEDs in the current unpredictable macroeconomic environment. The new and emerging risks and […]

Last October, the European Central Bank (ECB) initiated the preparation phase of the Digital Euro project, following two years of investigation and a proposal on the establishment of a digital euro published by the European Parliament (EP) in June 2023. In January, the ECB began seeking potential providers to develop a digital euro platform and infrastructure […]

The European Central Bank (ECB) issued the SSM supervisory priorities for the 2024-2026 cycle on 19 December 2023. They sum up what institutions under the direct supervision of the ECB should expect in terms of areas of supervision, in 2024 notably, and allow firms to prepare themselves for forthcoming onsite inspections or thematic reviews. Please […]

In January 2024, the European Central Bank (ECB) published its Climate and Nature Plan for 2024-2025. This plan aims to: This plan underscores those financial risks stemming from climate change remain a key area of attention for the ECB. The ECB will continue working on several topics including stress testing, scenarios and climate-related data, and […]

DORA is a legislative proposal that aims to improve the digital operational resilience and ensure the performance and stability of the financial system of the member countries of the European Union in the face of the risks associated with ICT (Information and Communication Technology) in the financial sector (cyber-threats, cyber-attacks). The DORA requirements will apply […]

In late 2023, and to coincide with COP 28, Mazars published its latest Sustainability practices survey on the progress banks and insurers have made in embedding sustainability into their businesses, our most comprehensive and information-rich report to date covering 404 executives in banks and insurance companies in 16 countries. Despite sustainability being in the limelight […]

The Single Resolution Board (SRB) convened its annual conference on 13 February 2024 with a theme highlighting the focus for the year: ‘The road ahead: risk, readiness and resilience’. While significant strides have been made with the EU banking resolution framework and tools, the SRB’s Chair Dominique Laboureix recalled this is not the end of […]

In environmental, social and governance (ESG) reporting, materiality is crucial for enhancing transparency and accountability in sustainability and climate-related disclosures. Importantly, it helps identify and report on matters that are deemed significant, emphasizing their relevance to stakeholders. Materiality comes in various forms. Financial materiality focuses on sustainability issues impacting financial performance, aligning with annual financial […]

To adapt to the swiftly evolving regulatory landscape and meet stakeholders’ expectations, financial firms are increasingly formulating sustainability strategies to address environmental, social and governance (ESG) factors. Notably, emissions reduction and the pursuit of net-zero targets have become central elements of ESG strategies for many financial firms, according to the latest Mazars’ survey Sustainability practices stocktake: […]

On 29 June 2023, the European Union’s (EU) Markets in Crypto Assets Regulation (MiCA) entered into force. It is being implemented in stages depending on the provisions, between June and December 2024. The regulation, which provides clearer rules for crypto-asset service providers and token issuers, is much needed for this fast-changing industry. The rapidly approaching […]

The integration of environmental, social and governance (ESG) considerations into strategic planning is increasingly becoming a common practice among financial services firms. However, climate-related risks can also serve as drivers of financial risk for institutions. These risks can manifest through various transmission channels, translating climate and environmental (C&E) risks into more conventional categories such as […]

There is growing pressure for banks and insurers to incorporate C&E factors in their risk management frameworks (RMF). As a practice, it gives the ability to set clear thresholds for the climate impacts banks and insurers are willing and able to absorb. By establishing these thresholds, firms can effectively monitor their exposure to C&E risks, […]

There are increasing regulatory expectations globally for financial institutions to disclose and demonstrate how sustainability-related responsibilities are allocated within the organisation. In this respect, the increasing global trend towards mandatory sustainability disclosure frameworks continues to underscore the significant role that the finance function is anticipated to assume in sustainability. It’s a trend reflected in Mazars’ […]

On 19 December 2023, the European Central Bank (ECB) published its updated Single Supervisory Mechanism (SSM) strategic supervisory priorities for the period 2024 to 2026. The priorities indicate what banks should expect in terms of supervisory activities in 2024. For 2024-2026, the ECB supervisory priorities are built upon three main pillars: These priorities were informed […]

The increased demand for sustainable finance shows that awareness of environmental, social and governance (ESG) issues is generally high among financial institutions. Indeed, for many of the larger players subject to the EU’s Non-Financial Reporting Directive (NFRD), there has been a requirement to include ESG information in annual reports for some time. Others have incorporated […]

While the banking sector has shown resilience over recent years, the economic environment and geopolitical situation remain tense. So, what does this mean for risks to the banking sector? More specifically, what is the impact on capital requirements for banks with the implementation of the Capital Requirements Regulation (CRR3) and the Capital Requirements Directive (CRD6), […]

The Basel Committee on Banking Supervision (BCBS) and Financial Stability Board (FSB) published reports in October 2023 on the causes and lessons learnt from the Spring 2023 banking turmoil. The BCBS report provides an assessment of the causes of the banking turmoil, the regulatory and supervisory responses, and the initial lessons learnt. The FSB report […]

The implementation of the European Union’s ‘Taxonomy’ regulation, which integrates two climate objectives, was carried out on 1 January 2022 through the ‘Climate’ Delegated Act released in April 2021. In line with this, the banking sector has been provided with corresponding regulations, allowing banks to measure the portion of their financing dedicated to sustainable economic […]

In 2022, the European Union implemented the green taxonomy for the second year, requiring companies to disclose indicators related to climate objectives. The green taxonomy aims to guide capital investment towards environmentally sustainable activities, making companies assess their alignment with the EU’s sustainable transition and enabling financial institutions to prioritise funding for projects contributing the […]

2023 marks the second year in which insurance and reinsurance companies have published their eligibility ratios for the European Green Taxonomy. For the insurance sector, the objective is to measure the proportion of investments, as well as the proportion of gross premiums collected in non-life insurance, dedicated to financing economic activities in accordance with the […]

The IIF Annual Membership meeting is a setting for insights and perspectives from global financial regulators and senior financial sector executives on topical economic and regulatory issues. Being a forum with global coverage means that it is a valuable setting for picking up future economic and regulatory directions. A packed agenda under the theme of Building […]

DORA (the Digital Operational Resilience Act) is the key regulatory outlook for IT and Cyber risk between now and 2025. The European Supervisory Agencies have sought to strengthen the resilience of institutions by emphasising the need to evolve the approach to operational risk management, of which information and communication technology risks are a part. DORA […]

Under IFRS 9, forward-looking information is a key component of Expected Credit Loss (ECL) calculations. However, forward-looking information requires a significant level of judgement, making comparisons difficult to navigate. Indeed, similar to the use of post-model adjustments, forward-looking scenarios have also been reported by stakeholders in the context of the IFRS 9 impairment post-implementation review […]

Despite banks emerging from the Covid-19 crisis in reasonably good health, the war in Ukraine combined with a global energy crisis and an uncertain economic landscape have once again put the spotlight on credit risk exposures. To better understand credit risk trends, Mazars conducted an analysis of 26 banks in 11 European countries in May […]

Since the Covid-19 pandemic, post-model adjustments1, or management overlays, have become an increasingly common and accepted mechanism used by banks to manage expected credit losses (ECLs). The number of post-Covid unprecedented events related to the war in Ukraine, energy crisis and global economic uncertainty has raised a number of questions relating to the consistency and […]

A recent major board reshuffle in one of Europe’s largest listed investment companies has focused attention on private investment valuations. It follows concerns raised by an ex-director over the robustness of the directors’ processes for approving investment valuations. The issues primarily question whether the Board of Directors has sufficient training and experience and whether governance […]

Revised list of uncooperative countries and territories for tax purposes published by the European Council The list of uncooperative countries and territories about tax is an important part of the external tax strategy of the EU. Globally, this strategy intends to contribute to the ongoing efforts to advance good governance practices in the tax domain. […]

ACPR publishes report on automated AML/CFT transaction monitoring systems In 2022, the ACPR conducted a comprehensive thematic review, focussed on the automated systems utilised by the entities under its supervision. This entails entities implementing their obligations in terms of transaction monitoring. The primary objective of this review was to assess the efficiency of the operation and […]

The Eurofi financial forum is a setting for exchanges between European Union (EU) economic and financial regulators and senior financial sector executives from the industry. It occurs bi-annually alongside the Economic and Financial Affairs Council configuration (ECOFIN) meetings. This summary takes stock of the Eurofi discussions, as well as recent publications by the EU Commission […]

2022 AML-CFT Committee report available The MONEYVAL Committee, an entity of the Council of Europe which is tasked with addressing challenge of money laundering and terrorist financing (ML/FT), has recently published the AML-CFT report 2022. The findings of the report are primarily centred around adherence to compliance with global sanctions, notably in freezing or confiscation […]

With the approaching end of the investigation phase of the ECB’s digital euro project in October 2023, and the expectance of a decision on starting a realisation phase by the end of this year, the pros and cons of a potential digital euro have been widely discussed in the past months. The topic became even […]

New report on AML/CFT risks in payment institutions In accordance with the European Union regulations, the European Banking Authority (EBA) has been mandated to assess the management of the most significant risks in the fight against money laundering and terrorist financing (ML/FT). The entity’s analysis is centred around the identification and management of ML-FT risks […]

New measures to combat money laundering and terrorist financing The European Parliament has adopted a set of stringent measures to strengthen the fight against money laundering and terror financing, alongside circumventing sanctions within EU. These regulations are presented by EU in the form of a “legislative package” comprising three key measures which provide various practical […]

ESG-related regulatory requirements, and scrutiny, show no signs of abating. Asset managers have a pivotal role in financing the transition towards low-carbon economic systems. Hence, governments have introduced several ESG-related regulatory requirements that apply to asset managers. Some examples of these are the Sustainable Finance Disclosure Regulation (SFDR) in the EU and the mandatory disclosures […]

Both the UK and the EU are consulting on the next wave of iterations to the Basel reforms. Whilst the focus of these consultations has been relatively broad, the rules around the computation of Pillar one Credit Risk RWAs have seen the most significant change. This article outlines some of the main differences between the […]

The European Commission published on 18 April 2023 a new legislative package aiming to adapt and strengthen the framework for crisis management and deposit insurance (CMDI), with an acute focus on small and medium-sized banks. This proposal, which follows the announcement of the Eurogroup finance ministers inviting the Commission and the European co-legislators to review […]

On 16 December 2022, the AMF published additional information[1] on its website about the AMF exam, more commonly known as the “AMF certification” exam, since it certifies only the entities that organise the exam, rather than the people who pass it. The AMF lists the various functions within ISPs and FIAs that are covered by […]

The tax system applicable in the overseas public authorities includes a set of investment incentive schemes designed to promote their economic and social development. One factor to their successful implementation in practice is to provide as much visibility and sustainability for an investor as possible over time. Another key is to have a broad scope […]

The European Securities and Markets Authority (ESMA) published on 17 November, together with EBA and IOEPA, a Q&A on the RTS of the SFDR Delegated Regulation (Commission Delegated Regulation (EU) 2022/1288), just six weeks before coming into force. The Q&A clarifies a number of points, including those relating to principal adverse impacts (PAIs) and taxonomic […]

In recent weeks, we have witnessed the successive bankruptcies of three banks in the United States, as well as the hasty takeover of Credit Suisse by UBS. This chain of events inevitably calls into question whether this trajectory echoes the leadup to the financial crisis of 2008. In reality, whilst these crises have stark similarities, […]

Since the onset of 2023, regulatory news has been adorned with the latest European legislation, under the acronym DORA, adopted on 10 November 2022 by the European Parliament. Standing for the Digital Operational Resilience Act, it will apply to the members of the European Union from 2025, and concerns companies in the financial sector specifically. […]

The momentum towards a low-carbon economic system is only set to grow. Financial services firms are pivotal actors in the transition; consequently, increasing demands are being put on them to demonstrate their sustainable finance activities and credentials. This blog explains what sustainable finance is and why it matters to financial services firms. What is Sustainable […]

Implementing credible environmental, social and governance (ESG) actions requires successful enablers. So how can firms identify these enablers and, crucially, remove barriers to implementation? If we take our latest C-Suite Sustainability Barometer, we can see that out of the over 1,100 businesses accounted for in the survey, 75% are planning to increase their investment in […]

“I see digital as the future of finance”. These are the words of the Executive Vice President of the European Commission (EC), Valdis Dombrovskis, voiced in the summer of 2020. He has undoubtedly been proven right as governments and central banks around the world have heightened their efforts to keep oversight of the digital transition […]

The global climate crisis has triggered the financial sphere to address the way in which it conducts business. Climate risk consideration is currently growing in the banking industry but should also be considered by banks in the Credit Valuation Adjustment (CVA) when pricing derivatives. The credit risk for long dated derivatives (beyond 10 years), reflected […]

The Federal Reserve Board (Fed) has shared instructions on its pilot climate scenario analysis exercise (CSA). Six of the largest U.S. banks, i.e., Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley, and Wells Fargo are participating in the exercise and are requested to submit their results along with documentation by July 31, 2023. […]

In our last article on sustainability-linked financing, we highlighted the accounting issues related to these contracts that are currently being debated between stakeholders. The most critical issue is the classification of loans or bonds that reference the borrower or issuer’s environmental, social and governance (ESG) key performance indicators (KPIs) on the balance sheet of lenders […]

After two years marked by the Covid-19 crisis, the first half of 2022 offered the prospect of a return to a certain economic normality. However, the outbreak of war in Ukraine combined with a deteriorating economic environment have reshuffled the cards and once again brought banks into a zone of turbulence and uncertainty. So how […]

A lot of attention at COP27 was focused on the likelihood of keeping global warming to 1.5 °C, in line with the goals of the 2015 Paris Climate Agreement. The consensus was that we are in real danger of falling off track. Few nations revised their nationally determined contributions to reduce their carbon footprint compared […]

The European Central Bank (ECB) has expressed a significant supervisory concern surrounding more than half of supervised banks in terms of the progress made on fulfilling the expectations specified in the Guide on climate-related and environmental risks. The ECB recently concluded its 2022 thematic review of the banking sector’s alignment with supervisory expectations. This review […]

The European Banking Authority (EBA) is tasked, in cooperation with the European Systematic Risk Board (ESRB), to initiate and coordinate biennial EU-wide stress testing exercises to assess the resilience of institutions to adverse market developments. The objective is to provide supervisors, banks, and other market participants with a common analytical framework to consistently compare and […]

As environmental, social and governance concerns are becoming more and more prevalent, sustainable finance is now under the spotlight. The financial sector has a key role to play in achieving the ESG transition. One of the levies developed by the financial industry is to propose new kinds of financing that promote ESG practices and projects […]

The European Union (EU) has taken the first step in directing capital investments toward so-called sustainable activities with the introduction of the Green Taxonomy on 1 January 2022. For the real estate sector, the objective is to measure the share of eligible activities contributing to the first two climate objectives – the mitigation of climate […]

In summer 2022, the Bank for International Settlements (BIS) published its second consultation paper on the prudential treatment of cryptoasset exposures. The guidelines outlined in the proposed document follow an initial discussion paper released in 2019 and a first consultative document issued in 2021. The complete text is set up as a new standard to […]

The Federal Reserve Board (FED) will commence its first bottom-up climate scenario analysis exercise at the beginning of 2023, as announced on 29 September. The exercise will be exploratory in nature and will not result in extra capital requirements. The list of designated participants consists of six of the largest U.S. banks, i.e., Bank of […]

The objective of the European Union’s Taxonomy regulation, in force since 1 January 2022, is twofold for the insurance and reinsurance sector. First, to measure the share of investments devoted to financing economic activities eligible for the taxonomy, known as the Investment Ratio. Second, to measure the share of gross premiums written in eligible non-life […]

In force since 1 January 2022, the European Union’s Taxonomy regulation aims to support the market for green finance. More specifically, greater transparency in the market will help prevent greenwashing by providing information to investors about the environmental performance of assets and economic activities of financial and non-financial information. For the banking sector, the target […]

A new regulation introducing a pilot scheme based on blockchain technology is set to come into force on 23 March 2023. The new European regulation1 is an experiment to develop secondary markets for financial securities based on distributed ledger technology (DLT). Authorised participants in the scheme will be able to provide trading services and settlement-delivery […]

The first supervisory climate risk stress test (2022 CST) conducted by the European Central Bank (ECB) has concluded with official results and findings made public on 8 July 2022. The exercise has complemented the broader ECB’s agenda to assess the readiness of banks in Europe to manage climate-related and environmental risks. The 2022 CST was […]

Following Russia’s annexation of Crimea in March 2014, the United States (US) and the European Union (EU), together with other countries, imposed mainly economic sanctions on Russia. Since Russia’s recognition of the self-proclaimed autonomous republics of Donetsk and Lugansk, followed by Russia’s attack on Ukraine on 24 February 2022, these sanctions have taken on new […]

Climate change is now firmly in the focus of prudential regulators and supervisors across the globe. Against this background, the European Banking Authority (EBA) is mandated to assess whether a dedicated prudential treatment of exposures related to assets or activities associated substantially with environmental and social objectives would be justified. Based on its findings, the […]

The last few weeks have been marked by an ongoing review of the supervisory priorities initially listed by the Single Supervisory Mechanism (SSM) for 2022-24, and developments in the climate agenda outlined by the European Central Bank (ECB). ECB’s supervisory priorities for 2022-24 remain stable despite geopolitical instabilities and challenges At the beginning of 2022, […]

For several months now, we have been in an economic and financial environment that we have not seen for some years. In May, inflation in the Eurozone reached 8.1%, with six countries exceeding 10%, while the United States recorded an 8.6% year-on-year price increase. The short-term reasons for the return of inflation are well known, […]

The years between 1848 and 1918 are considered the relevant building period for the Gründerzeit-Zinshaus buildings in Vienna. In this period Viennese housing construction underwent a decisive development which shaped the city’s characteristic flair to this day: the Zinshaus buildings – so typical for Vienna – came into existence. Viennese Gründerzeit-Zinshaus buildings have not lost […]

France’s innovative and incentivising Action Plan for Business Growth and Transformation (PACTE) law lays the legal foundations for corporate social responsibility. With more than 400 companies established as “sociétés à mission” – mission-led businesses – by the end of 2021, this new scheme is an undeniable success. The number of mission-led companies has doubled in […]

Central Bank Digital Currencies (CBDCs) continue to receive increasing attention not only from the ECB but all over the world. So far, 10 countries [1] have already deployed CBDC programmes with another 15 countries [2] currently conducting pilot programmes. In total, 105 countries are considering using CBDC programmes, representing over 95% of global GDP and […]

The chair of the European Central Bank’s Supervisory Board, Andrea Enria, has voiced several times in the past months the supervisor’s concern with the increasing growth of the leveraged finance sector, which deals with loans to highly indebted borrowers. By mid-2021, the combination of a strong global loan moratoria policy and the long-standing low interest […]

The war in Ukraine, as well as the unprecedented sanctions imposed by the European Union, the United States and their partners against Russia have had major consequences for financial services institutions. For foreign companies operating in Russia or Ukraine, the first concern was the safety of their staff. They had to make difficult choices to […]

While the European Commission’s most recent opinion on the review of the Solvency II Directive is broadly in line with the final European Insurance and Occupational Pensions Authority (EIPOA) opinion issued in December 2020, some measures have now been amended. These amendments are designed to strengthen the capacity of European insurers to contribute to the […]

Regardless of geography or business sector, many groups and companies have taken out cybersecurity insurance policies in recent years. These policies cover companies against new threats to information systems, including ransomware and data theft incidents that have been making the headlines. For a long time, the risks identified in these policies were on the borderline […]

The European Green Deal aims to achieve climate neutrality by 2050 and create a modern, competitive and resource-efficient economy. To meet its objectives, the European Commission has begun to restructure the non-financial reporting requirements for companies. Although some of the requirements were partially implemented in 2021, this is only the beginning of a real sea […]

Since the European crisis management framework was established in 2014, there have not been many failing banks in Europe. However, the recent global health pandemic, combined with the ongoing conflict in Europe between Russia and Ukraine, could easily change this. The EU crisis management framework was established in response to the global financial crisis and […]

Crypto-asset markets have been on banks’ radar for some time. While interest and involvement have varied, regulatory developments have been a driving force. In September 2020, the European Union (EU) published a proposal for the regulation of Markets in Crypto-assets (MiCA), offering a uniform legal framework for crypto-assets in the EU. On 14 March 2022, […]

As a setting for exchange between European Union (EU) economic and financial regulators and senior financial sector executives from the industry, one of the world’s largest financial services conferences, Eurofi, took place in Paris in February. Established in 2000, the Eurofi meetings occur bi-annually* alongside the Economic and Financial Affairs Council configuration (ECOFIN) meetings. The […]

In March 2022, the European Central Bank (ECB) published its second snapshot of climate-related and environmental risk disclosure levels among significant institutions under its direct supervision. In line with the results of the first snapshot published in November 2020 – regarded as the baseline measurement – none of the institutions in scope for this second […]

The invasion of Ukraine by Russia on 24 February 2022 is considered the most significant geopolitical event since the Second World War. While there is no question of military intervention by the European Union (EU) at the moment, the EU has nevertheless decided on a major package of sanctions that will have a heavy impact […]

A central database to strengthen the anti-money laundering and counter-terrorist financing (AML/CFT) framework was launched by the European Banking Authority (EBA) on 31 January 2022. Called EuReCA, the new database will be essential to coordinate efforts by national competent authorities and the EBA to prevent and fight money laundering and terrorist financing (ML/TF) risks throughout […]

Like all industries, the real estate sector has to implement a range of legal, technical and organisational measures to protect the personal data of its employees, customers, prospects and suppliers. Processing must comply with several regulations related to data protection, including, for example, the General Data Protection Regulation (GDPR), applicable since 25 May 2018. Same […]

As part of the European Green Deal, the European Union intends to encourage green investments and prioritise the revision of the Non-Financial Reporting Directive (NFRD). The European or Green Taxonomy, which sets out a precise classification of sustainable activities with the strategic objective of redirecting capital flows towards those activities from 2022, is a result […]

The market is seeing a growing trend for real estate management companies seeking to speed up the process of closing their accounts. This is largely due to the positioning of real estate funds in life insurance contracts requiring increasingly shorter valuation intervals. Furthermore, as the regulatory obligation to publish Net Asset Values (NAVs) within the […]

As part of its rotating Presidency of the EU Council for a six-month mandate, France chaired its first EU Council of Finance Ministers (ECOFIN) meeting on 18 January with a view to getting certain current legislative work finalised. The ECOFIN meeting was mainly dedicated to introducing the Presidency’s roadmap for the months to come. Beyond […]

As regulated entities execute their post-Brexit strategies and relocate their European Union (EU) operations from the UK to other EU states, a key issue to be addressed for those relocating to Ireland remain to be the impending legislative changes surrounding increased accountability standards for executives and non-executives. Not least, the breaking of the participation link, […]

The great financial crisis triggered a massive wave of bankruptcies in the worldwide banking sector, affected not only large international banks such as Lehman Brothers but also local ones such as Northern Rock in the UK. Basel prudential standards are designed to cope with financial risks stemming from the global banking system without taking into […]

Supervisory priorities 2022-2024 In December 2021, the European Central Bank (ECB) and the national supervisory authorities of the Eurozone countries published their supervisory priorities for 2022-2024. The three-year coverage enables the ECB banking supervision to achieve good progress in addressing the identified vulnerabilities while at the same time affording enough flexibility in any corresponding actions […]

The growing importance of sustainability issues and the role of credit institutions in financing transformation places climate and environmental risks at the core of regulatory and supervisory scrutiny today. For some years now, the Network for Greening the Financial System (NGFS), comprising central banks and national supervisory authorities, has been working to enhance sustainability and […]

Financial institutions and non-bank financial technology companies (FinTechs) alike make extensive use of various machine learning models (MLOps) in core and non-core areas of their business. Banks, for example, rely on such models for a range of risk assessments, including predictive underwriting, credit risk management, suspicious and/or fraudulent activity management, fair lending compliance, derivative and […]

The Covid-19 pandemic has amplified technology’s impact on the banking sector, helping to prove that technology now stands at the core of business sustainability for banks. In their constant search for convenience, digitally-savvy customers have pushed banks’ focus towards providing global business solutions more than ever. A new normal has emerged: an environment where banks’ […]

The creation of a new Anti-Money Laundering Authority will transform the supervision of money laundering and financing terrorism (AML/CFT) in the EU. Proposed reforms also extend the AML/CFT rules to all crypto-asset service providers, as well as include specific rules concerning due diligence on customers and beneficial ownership. It is expected that some of these […]

On 22 September, the European Commission adopted a review of Solvency II following the consultation launched by EIOPA in 2020, whose final guidance was published in December 2020. As the Commission notes, the 2020 review of the directive met several objectives: • remove the obstacles to long-term financing of the economy and redirect investment by […]

The Financial Stability Oversight Council (FSOC) was established under the Dodd-Frank Wall Street Reform and Consumer Protection Act as a result of the 2007-2008 US financial crisis. A first of its kind, the 15-member council is tasked primarily with identifying growing systemic risks to US financial stability and proposing coordinated regulatory responses to both preempt […]

The widespread use of working from home (WFH) during the pandemic, regardless of sector or geographical location has required organisations and their information systems (IS) management to be very agile in deploying or increasing their capacity for remote collaboration. Some institutions were already prepared – for example, following the wave of strikes at the end […]

As the PRA transitions from a “rule-taker” to a “rule-maker”, small and medium-sized banks operating in the UK can expect to benefit from a more “streamlined” regulatory regime that could be easier to interpret, implement and maintain; but at the same time, they can also expect the PRA to be progressively more involved in scrutinising […]

The identification and management of non-performing loans or NPLs as early as possible by banks are among supervisors’ current high-level priorities. Indeed, when prudential, monetary, and fiscal crisis mitigation mechanisms are tapered, the weakening of borrowers’ creditworthiness could materialise, along with increasing credit risks and therefore NPLs. This expected rise of new NPLs in European […]

The unveiling of the new banking package “CRR3 – CRD6” on 27 October 2021 presents a further landmark on the road to implementing the final Basel III agreements. The regulatory scheme will also focus on the revision of the market risk framework from January 2019, as well as the latest developments in pillar 3 requirements. […]

The low level of banking consolidation in Europe compared to other countries is raising concerns among the supervisory community in Europe. It is a trend further reinforced after the financial crisis of 2007/2008 that produced a noticeable slowdown in consolidation operations in the EU. So what has been the impact, and what can we expect […]

Climate change introduces considerable economic challenges. On the one hand, financial institutions must contribute to the transition to a low-carbon and balanced economy to effectively combat global warming. On the other hand, the financial sector is exposed to climate-related and environmental risks and therefore needs to implement appropriate risk management practices within a financial stability […]

On 30 July, the European Central Bank unveiled the 2021 supervisory stress test results, which demonstrated that the region’s banking system is resilient in an unfavourable environment. The Common Equity Tier 1 (CET1) ratio has fallen 5.2% to 9.9% under the 3-year adverse scenario, while under the baseline scenario the CET1 ratio will reach 15.8% […]

The continued popularity of funds with an environmental, social and governance (ESG) focus has put global ESG assets on track to exceed $53tn by 2025, up from nearly $38tn at the end of 20201. As growth continues, expectations for effective compliance policies and controls in place are expected to become more rigorous as political and […]

A growing interest in environmental, social and governance (ESG) issues is driving record inflows into the ESG-led investment sector. During 2020, sustainable funds available to European investors attracted net inflows of €233bn1, which saw assets under management hit the $1.1tn milestone, accounting for almost 10% of total European fund assets. A similar growth story in […]

The recent breakthrough of data science and deep learning make a model independent approach for hedging possible. This hedging approach known as deep hedging is a robust data-driven method able to consider market frictions as well as trading constraints without using model-computed greeks. This article gives the main theoretical tools to understand the methodology and […]

A major step forward has been taken in implementing the European “investment firms” package in France*. The transposition of the package into local legislation, alongside EU Regulation 2019/2033 on prudential requirements for investment firms (IFR), came into full effect on 26 June 2021. In accordance with the proportionality principle, the IFR and investment firms directive […]

Recently, initiatives to tackle climate-related and environmental risks in the financial services industry have begun across the world. These initiatives followed the adoption of the United Nations Paris Agreement on climate change, the 2030 agenda for Sustainable Development and the European Green Deal. Stress testing and scenario analysis are a common framework proposed by different […]

Local and international trends have transformed the way banks operate, affecting their capital positions and profitability. In particular, ongoing digitalisation programmes and technological innovation continue to add pressure on traditional banking models, including the supply chain. While management’s focus on capital preservation, profitability and growth for shareholders remains, risks from an operational perspective have intensified. […]

With the current ultra-low interest rate environment and market volatility having a negative impact on banks’ returns and, ultimately, their capital positions, operating models must quickly adapt and become more cost-efficient to maintain profitability. This drive for cost-efficiency has become more apparent as innovation in technology and ongoing digitalisation have further upended traditional banking systems […]

Brexit, or the UK’s departure from the European Union, became a reality on 1 January 2021. In terms of the regulatory impact for the financial sector, and the banking sector in particular, the UK being a third country, UK banks can no longer benefit from the European passport for their continental activities. Therefore, they can […]

On 1 March 2021, the European Banking Authority (EBA) launched a public consultation on draft implementing technical standards (ITS) for Pillar 3 disclosures of environmental, social and governance (ESG) risks, under its capital requirements regulation (CRR) mandate. The consultation will end on 1 June 2021. Large banking institutions with securities traded on a regulated market […]

The digitalisation of banking processes and the introduction of AI-led technology impact the central and strategic role of information systems within the banking system. The growing use of information and communication technology (ICT) exposes all financial institutions to an increasing level of digital risk that could weaken their operational resilience, in particular, due to more […]

The Targeted Review of Internal Models (TRIM) was one of the largest projects by the European Central Bank (ECB) aimed at identifying potential sources of unwarranted or non-risk based variability in Significant Institutions (SIs) risk-weighted assets (RWA) from the use of Pillar 1 internal models such as Probability of Default (PD), Loss Given Default (LGD) […]

Click here to read ‘Key takeaways & industry challenges following the ECB TRIM project – a focus on credit risk (Part 2)’ As articulated by the ECB in its recent TRIM reporting, the 236 findings cover different key aspects of supervised entities Internal Model Method (IMM) models & frameworks. Remediation actions are underway in all […]

Against the background of a new year still severely affected by the persistence of the pandemic throughout the world and economies facing an unprecedented global macro-economic shock, the Basel Committee has felt it necessary to address the audit of the expected credit loss (ECL) accounting estimate within the overall financial statement audit. With IFRS 9 […]

Over the past decade, the financial services industry has been disrupted by the arrival of new players whose rise to prominence has pushed traditional banks – previously faced with little competition – to transform themselves. In this context, technology and innovation, particularly 5G, will allow the most skilful and agile banking organisations to take advantage […]

While 2020 went relatively smoothly for the banking sector, uncertainties remain on the potential effects of Covid-19 on the real economy. Any negative impact could lead to heavy losses for the sector, especially when support measures are gradually phased out. These measures have not only contained the anticipated increase in credit risks, but have also […]

On 13 November 2020, the EBA published the final methodological note for the 2021 EU-wide stress-testing exercise. The aim of the stress tests is to assess the resilience of financial institutions to adverse economic and financial developments, in particular in the event of an increase in credit risk due to the default of the borrower. […]

The publication on 29 January of baseline and adverse scenarios, output templates, instructions and market assumptions required to carry out stress tests signals the go-ahead by the European Banking Association (EBA) for the 2021 regulatory exercise. Because of the Covid-19 pandemic, these tests, originally planned for 2020, will take place between now and 31 July […]

With the economic repercussions of the Covid-19 crisis yet to be fully assessed, a robust resolution framework is essential to ensure the stability of the banking system. While the banks were given leave to postpone the reporting of some less urgent information in spring 2020, the Single Resolution Board (SRB) has reiterated the importance of […]

While there is a consensus about the smart building concept, there are still challenges to overcome if tomorrow’s buildings are enhanced to benefit the environment, cities and people. Starting with their design and throughout their useful lives, buildings have a huge impact on the environment and the quality of life of their users. So how […]

While digital transformation has been disrupting all business sectors for many years, 2020 will be remembered for its particular impact on real estate administrators. A third of French respondents believe that artificial intelligence can be more efficient than a real estate agent. Moreover, 40% of those under 50 years old are convinced that the property […]

European sustainable finance regulations evolved considerably in 2020, and the European Banking Authority (EBA) is continuing this trend into 2021. It recently published a discussion paper assessing the potential inclusion of Environmental, Social and Governance (ESG) risks in the supervisory review and evaluation process (SREP) performed by national competent authorities (NCAs)[1]. What firms need to […]

With more than half of the world’s fastest-growing economies located in Africa1, the continent’s economic outlook is a positive one. Average annual GDP growth since 2000 is over 5%, placing Africa as the second-fastest growing economy behind Latin America. Real GDP growth, estimated at 3.4% for 2019, is projected to accelerate to 4.1% in 2021. […]

This article is part of the series covering the impact of sustainable finance on the insurance sector. Read further:Part 1: Assessing the impact of sustainable finance on insurance entitiesPart 2: How the insurance sector is meeting ESG challenges Clarity of information provided to various stakeholders is a growing issue for financial organisations. Despite the efforts […]

This article is part of the series covering the impact of sustainable finance on the insurance sector. Read further:Part 1: Assessing the impact of sustainable finance on insurance entitiesPart 3: Developing a toolkit for responsible investment decisions When taking environmental, social, and long-term asset portfolio issues into consideration, insurance companies must assess the specific risks […]

This article is part of the series covering the impact of sustainable finance on the insurance sector. Read further:Part 2: How the insurance sector is meeting ESG challengesPart 3: Developing a toolkit for responsible investment decisions Amid a global pandemic and a rising threat of climate change, today’s society expects financial organisations to uphold strong […]

The working environment has always been an important factor for companies’ performance and their ability to attract talent. With the rise of remote work, this aspect has become critical: companies now have to ‘seduce’ staff to return to the office. Therefore, real estate services will play a crucial role in helping businesses upgrade working environments […]

The global real estate crowdfunding market was estimated at USD13.2bn in 2018 and is expected to reach USD868.9bn by 20271. In addition, the market is expected to grow at a compound annual growth rate (CAGR) of 58.3% from 2019 to 20271. In Europe, excluding the UK, real estate crowdfunding transaction value was USD600.1m in 20182. […]

In this edition of our Banking Regulatory Radar, we cover the key regulatory developments in the banking sector for 2020-2025. The latest version of the Mazars’ Regulatory Radar has been updated with all the Level 2 legislation published in 2020, as well as the measures that were taken in the context of the Covid-19 pandemic. […]

Facebook’s ambition to create a transferable global digital coin between users on the social media giant’s messaging platforms WhatsApp and Messenger has been controversial from the outset. Perhaps not surprisingly, the backlash from regulators around the world was substantial from day one. The world’s leading economies were less than enthusiastic of the possibility of a […]

The pandemic has had a significant impact on our entire ecosystem. We have seen global CO2 emissions fall by a record 7% in 20201 benefitting the environment. Yet, at the same time, we have seen adverse consequences for the mental health of staff working remotely, with almost half (49%) of those working from home saying […]

March 2020 marked the first time – since its inception in 2014 – that the Bank of England (BoE) cancelled its annual stress tests for the UK’s biggest lenders. Instead, they undertook a desktop analysis of the UK banking sector resilience. In late 2020, the Financial Policy Committee (FPC) judged that most banks have capital […]

Around one-fifth of global banking activity is undertaken in the UK. Almost half of the UK’s banking assets are held by international banks. The PRA currently supervises approximately 250 international banks, both branches and subsidiaries, which are part of around 180 international groups. Background On 11 January 2021, the PRA shared in a Consultation Paper […]

One of the anticipated challenges in the transition from IBOR rates to risk-free rates (RFRs) is the management of its impact on quantitative models. The ones currently used for pricing IBOR-linked financial instruments account for term rates which are “forward-looking”. The RFRs replacing the IBORs are all overnight rates. This means that a term rate […]

Under article 430c of the updated Capital Requirements Regulation (CRR 2), the European Parliament and the Council of the European Union mandate that the European Banking Authority (EBA) perform a feasibility study on reducing the reporting burden for the European banking sector while ensuring data collection for monetary policy, resolution and supervisory purposes and take […]

There is little doubt that Covid-19 has had a significant impact on insurers, but there were already factors in play that were adding pressure on the insurance industry. What covid-19 has done is to create new challenges, as well as bringing existing challenges to the foreground. Looking ahead, the actions insurers take now to deal […]

An important milestone in the IBOR transition is the change in rates used by LCH and CME for discounting and Price Alignment Interest (PAI) calculations for USD OTC cleared swaps. Indeed, on October 16, 2020, they moved from using the daily Effective Federal Funds Rate (Fed Funds) to the Secured Overnight Funding Rate (SOFR) for […]

As the world gears up for the transition to net-zero, the European Union is setting ambitious targets with respect to its own environmental footprint. For instance, by 2030 the EU is looking to reduce European greenhouse gas emissions by at least 55% compared to 1990 levels; increase the share of renewables within Europe’s total energy […]

In the early 1990s, stress tests became a popular internal tool for international banks to examine risks and gain a better understanding of threats to the institutions’ balance sheet. From there, the Basel Accord was amended in the mid- ’90s and required banks and investment firms to conduct stress tests. However, these were more internal […]